As an auto insurance agent, a full pipeline is critical to your success.

It’s simple: The more high-quality leads you have access to, the greater chance there is of regularly closing deals.

In this guide, we break down the finer details of how to generate auto leads for insurance agents.

Upon completion, you’ll be more confident in your ability to generate leads, sell more policies, and boost your revenue.

Skip ahead: Check out auto insurance leads on Aged Lead Store

The benefits of purchasing auto leads

There’s no shortage of ways to generate auto leads.

From referrals to cold calling, your options run deep. In today’s market, buying leads is one of the best options. Let’s look at three reasons why.

1. Affordability

Don’t shy away from buying car insurance leads because of the price. Sure, it costs money upfront when compared to other options—such as cold calling or social media prospecting — but consider what you get in return.

Every lead you purchase is a driver who is interested in what you’re selling. This greatly improves the likelihood of making a sale with less stress.

2. Advanced filtering

Through filtering, you ensure that you’re only buying leads that suit your requirements.

Filtering options include but are not limited to lead type, states, age, zip codes, and carrier.

Use as many filters as necessary to buy leads that closely align with the coverage you can offer.

3. Comprehensive data

Buying leads is just the start. Making contact is critical to establishing a relationship.

With purchased leads, you receive the person’s phone number, email address, and postal address. This gives you several ways to contact them and stay in touch.

How much do auto insurance leads cost?

Return on investment (ROI) is the only thing that matters when buying auto insurance leads.

You want to earn more money than you spend on leads. Without this, you’re better off utilizing another sales and marketing strategy.

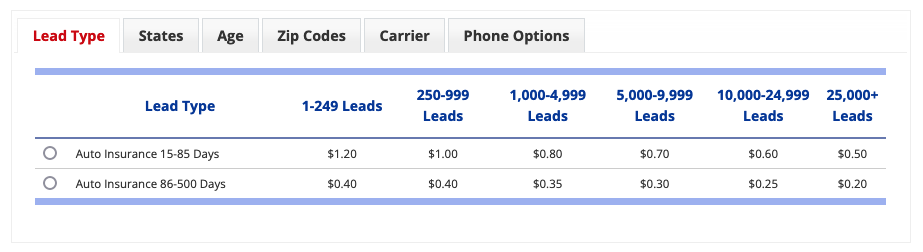

Calculating ROI starts with understanding the cost of aged auto insurance leads. The two details that impact price:

- Age: the older the lead, the lower the cost.

- Quantity: the more leads you purchase, the less you’ll pay per lead.

Take for example leads that are between 15 and 85 days old. If you purchase from 1-249 leads, your cost per lead is $1.20. With this, 200 leads would cost $240.

On the opposite end of the spectrum, purchasing 25,000+ leads comes at a cost of $.50/lead.

You may need to experiment with different types and quantities to find an approach that works with your schedule while providing the best potential for a positive ROI.

Keep your auto insurance pipeline full in 2023. Purchase aged auto insurance leads.

Top tips for selling to auto leads

Anyone can purchase auto insurance leads, but not everyone will make regular sales. Here are five tips for successfully selling to leads.

1. Don’t wait to make contact

Don’t buy more leads than you can comfortably afford to contact within 24 hours. Remember, you’re up against stiff competition.

The sooner you touch base, the sooner you show the consumer what you have to offer. Even if they’re speaking with other agents, you’ve at least “thrown your hat in the ring.”

2. Establish a solid foundation

Don’t expect to make a sale the first time you speak with a car insurance lead. It takes time to establish a solid foundation.

With this in place, it’s easier to gain the trust of the consumer. And when that happens, your chance of a sale increases exponentially.

3. Provide top-notch customer service

Customer service is a differentiating factor in the insurance industry. This holds true with both prospects and existing customers. Answer questions, provide guidance, and do your best to meet the needs of your audience.

4. Share more than one option

Don’t assume that every insurance lead knows what they want. There’s a good chance that they’re contacting you because they want to see what else is available to them. They’re leaning on you for professional guidance.

Upon reviewing and discussing their current and/or past coverage, share several policy options that you can provide them. For instance, you may want to talk about rental car coverage. It’s extras like these that can tilt the scale in your favor.

5. Stay in touch

When you buy auto insurance leads, be sure to do so from a provider that shares each person’s postal address, email address, and phone number.

This allows you to stay in touch via various means including phone calls, email messages, newsletters, and postcards.

Most sales don’t come after the first contact. Nurture your prospects through the pipeline from first contact to a closed deal.

Exclusive vs. non-exclusive leads

Exclusive leads are not shared between agents or agencies. They’re sold to one person, which increases your chance of a sale. On the flip side, since the lead is exclusive to you, it costs more money.

A non-exclusive lead is sold to more than one agent or agency. Competition is higher, but the cost is lower. The best way to combat increased competition is by making immediate contact with the lead.

If you have the time and budget, experiment with both exclusive and non-exclusive auto insurance leads. Use the same marketing ideas in both groups, track your results, and tweak your future approach accordingly.

10 great questions for your auto insurance leads

Asking the right questions of your lead can often win over the best sales pitch. This is true when selling to insurance leads, especially aged auto leads.

But not just any question will do. It has to be the right kind of question for the moment, and you should be thinking about how that question could advance your sales conversation—even before your prospect answers! Here’s what I mean.

We’ll handle the lead, you close the deal. Buy leads from Aged Lead Store.

Experiential questions can shift the transaction

A blog post by sales guru Seth Godin brought this idea home. Consider this familiar example:

Most [Girl] Scouts are taught to memorize a fairly complicated spiel, one that involves introducing themselves, talking in detail about the good work that the Scouts do, and finishing with how the money raised goes for this and for that.

This is difficult work even for a professional, but for a kid talking to an adult, it’s frightening and unlikely to lead to a positive experience. The alternative?

“What’s your favorite kind of Girl Scout cookie?”

In less than ten words, all the Proustian memories of previous cookie experiences are summoned up. In one simple question, the power in the transaction shifts, with the Scout going from supplicant to valued supplier.

The point here is that the right question can conjure up something in the buyer’s mind—an emotional memory, an experience, a desire, a feeling of happiness, pride, or even concern or worry.

The right question can shift the balance in your sales calls, getting your prospect to let down their guard, stop dwelling on price, and work with you, not against you, to meet their insurance needs.

Now, let’s move on to the questions.

Why are you shopping for insurance?

This is a classic “why” question, but with a very casual slant. You won’t raise as many eyebrows, and you could obtain some valuable information.

Car owners could change insurance all the time, but they don’t. The catalyst for this insurance query is the key to closing that sale.

How does your car manage winter weather?

People generally fall into two camps with the weather: they’ll tell you they avoid it, or they’ll feel proud about how well they are getting around. But the point isn’t so much the answer.

Whatever your prospect says out loud, they’ll privately conjure up the last time they skidded to a stop or saw a car in a ditch. With that picture in mind, their insurance coverage will seem more important to them.

Have you ever been rear-ended?

This is another question that’s not about the answer. It’s an indirect reminder that traffic accidents can happen to them even when they’re not moving.

What’s the worst accident you’ve seen?

Another good question, or line of questions, early in a sales call can be to ask about the lead’s experience with car accidents. They could tell you about an accident they’ve had, experienced as a passenger, driven past, or just read about in the news.

This is a very compact six-word question that can have a much bigger impact on your conversation than a longer script explaining the value of your insurance products.

Where do you work and what do you do there?

Often you’ll need to get a feel for who your lead is so that you can build a better relationship with them. People today spend a lot of time at work and often feel it’s a big part of who they are.

These kinds of personal questions help set you up for a better sales relationship. However, listen closely and take notes — you may also find an opportunity for cross-sales.

Do you take road A or road B to get to work?

Talking about work may allow you to talk about your shared community, too. A local interest question like this reminds your lead that you’re local, are a part of the same community, and can relate to them.

How long have you been married?

If a spouse or partner comes up in conversation, ask about them. You might learn that this person needs to approve the insurance purchase. Or you might hear a clue that leads to an eventual cross-sale.

Finally, this question is another way to get your lead to think about who they’re protecting with an insurance purchase.

What are your kids’ names? How old are they?

Asking about kids is another great tactic. Build a relationship with your lead by noting the kids’ names in your CRM and respectfully asking about them in subsequent calls.

Also, pay attention to the details — Is Junior starting high school? In another year or two, that may be an opportunity for a cross-sale.

What was the process like the last time you switched agents (or carriers)?

This is the perfect question for you to move the sale forward. If it was “easy” last time, signal that it will be easy this time as well. If it was a hassle, you have an open opportunity to explain how it will be a piece of cake this time around.

What type of coverage do you want?

This is an assumptive question that looks ahead to your client’s new ideal coverage, not backward at the unsatisfactory coverage they have now and that they’d rather leave behind.

This question also has the advantage of being very open. The lead can answer it however they want, and you can work to get them exactly what they ask for.

Sales scripts are great, but sometimes the perfect question does the work of a longer pitch more efficiently. Why make sales calls harder than they have to be?

These questions won’t sell Girl Scout cookies, but they will sell auto insurance.

Why choose aged car insurance leads?

Auto insurance lead generation boils down to two basic details: cost and quality. And that’s why aged leads are the perfect option for most agents.

Let’s start with the cost. As noted above, aged car insurance leads are more affordable than live leads. This is particularly true when dealing with leads that are 86+ days old.

As for quality, aged leads are the same as live leads. They are both drivers in the market for a car insurance policy. The only difference is that they submitted their information or quote request 15 or more days ago. Yes, there’s a chance that some consumers are no longer in the market, but that doesn’t affect the overall quality.

If you’re looking to purchase high-quality, affordable car insurance leads, consider those that are aged.

Conclusion on auto leads for insurance agents

By now, you should have a better understanding of all things related to auto leads for insurance agents. If you’re ready to take the first step in buying leads, visit our online store for more information.

Getting started is simple, but if you have any questions, contact us at 949-280-2548 for personal service.

Fill your sales pipeline fast and cheaply. Buy aged internet leads.